The page has been designed and written by Ayumi Ozeki ozekia@gmail.com

go to home http://ayumi01.s3-website-us-east-1.amazonaws.com

Cloud based simulation engine

This white paper describes the reengineering opportunities for

financial simulation engine utilizing Amazon SQS, AWS Lambda, Amazon

ElasticCache, and Amazon Redshift. Among varieties of cloud benefits, faster

results availability and pay-as-you-go model have unique implications to

simulation engine usage.

First let’s examine typical scaling technique used for simulation

engine. If you want to skip intro and go right to the Amazon Lambda based new

architecture section, click here.

Instant simulation result?

Generally speaking running simulation takes time to prepare, to run,

and to compile results. Vertical scaling (use of more powerful computer) and

horizontal scaling (adding nodes) will help completing the tasks faster. If we

can achieve performance gain where 10 times nodes mean 10 times faster job

completion, that suggests under the pay-as-you-go model it should cost the same

while achieving fastest time to delivery. When diminishing return on additional

node begins to materialize, however, the idea of provisioning massive nodes to

get the result instantly might not work too well. Considering the fact that

simulation involves processing the same routine as many times as the scenario

count with different simulated variables, such scaling conceptually works very

well, except there is a limit to this in reality.

Issues arise as scheduler gets busier and each node starts to have

varying degrees of the resource usage – i.e. increasing the node 10 times does

not mean 10 times faster unless each node uses identical resources, execute

same way, each task completion time being identical, and there is constant

coordination overhead. This is not the case. Many techniques exist to make it

efficient but perhaps the fundamental limitation is in its architecture of

distributing chunk of work to each node. Such “chunk of work” as a whole can be

quite complex, resulting in diverse resource usage across nodes. Scheduler gets

very busy finding available node to assign jobs and as such it gets very busy

as the node count gets higher.

The sections that follow will focus on end-of-the-day simulation-based

risk calculation as the basis of the discussion. Other types of the usage are

actually similar in architecture fundamentally. Let us first review the general

processes.

End-of-the-day financial risk calculation

The processes typically

happen in the following steps:

1.

Sourcing customer data

1.1.

Portfolio details

1.2.

Reference data such as customer’s risk rating and legal attributes that

affect risk attributes

2.

Gathering market factors

2.1.

Observable market data

2.2.

Derive additional data such as correlation and historic volatility from

observables

3.

Creating scenarios

3.1.

Simulate observable market factors

3.2.

Derive additional market factors from simulated ones

3.3.

Further derive the state of transaction set and reference data

4.

Pricing portfolios per scenario

5.

Determining expected value and stressed values of varying degrees based

on the scenarios

The most computationally intense part is step 4. Since there is no need

to complete it in a synchronous fashion it presents a great distributed

parallel processing opportunity. One possible distributed architecture is to

assign a task to a node in completing portfolio valuation per specific

scenario. A node may be assigned to do the routine for multiple scenarios –

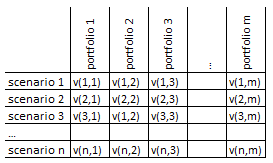

i.e. doing the similar calculation routine repeatedly. This table helps

illustrate ways a task distribution can be designed.

For example, a node may be

assigned:

-

By row slicing

o One or more scenarios and

valuation of all portfolios

o For a scenario valuation of

subset of portfolios

-

By column slicing

o Valuation of one or more

portfolios across all scenarios

o Valuation of one portfolio

under subset of scenarios

The idea is slicing the valuation needs by portfolio and by scenario,

and assign to each node accordingly. Again, asynchronous processing is

perfectly fine no matter how it is sliced. Before proceeding to the step five

to determine portfolio risks, all the valuation must be completed.

For a node to complete a

whole pricing of a portfolio – i.e. determining v(x, y) - it involves the

following computation steps:

1.

Given a set of instruments in a portfolio, determine necessary pricing

functions

2.

For each instrument that must be priced, determine market factors

required to price

3.

Retrieve unique set of market factors from a scenario, and price all

instruments in a portfolio

4.

Determine a portfolio price for the scenario

Distributed nodes typically perform all these steps by loading all

necessary pricing functions and required market factors. The node further runs

multiple valuation per scenario. As illustrated before, the job distribution by

portfolios and/or scenarios seems quite simple except across nodes, substantial

overlap in resource demands exist. For example, by scenario job distribution

means all nodes will load the identical portfolio data and pricing libraries.

In contrast, by portfolio job distribution means identical scenario data loaded

to all the nodes. Either way it appears inefficient.

Further decomposition below what has been illustrated is certainly an

idea – i.e. a node that specializes in pricing specific instruments, for

instance. The problem is now the scheduler. Each pricing engine requires

different sets of inputs and computation time requirement differs. A node that

specializes in FX forward pricing may finish all the work before more complex

credit default swap (CDS) engine has not even finished 10% of the work. A

scheduler can then assign next sets of CDS jobs to this idle node that used to

process FX forward. This process gets very complex and eventually becomes

inefficient as node count increases. It is inevitable idle resources pile up,

diminishing the return on additional node.

The prior section provided an example of how decomposition of processor

below portfolio valuation per scenario ends up creating scheduling challenges

and introducing diminishing return on additional nodes. This is where AWS

Lambda comes in.

AWS Lambda is a unique serverless architecture that is not available as

on-premise solution. You can’t just buy Lambda package and install on your

server. The fact that AWS Lambda executes code only when needed, scales

automatically, and as usual only pay for the usage while AWS takes care of

various underlying administration, it sounded like a magic wand in solving

typical simulation engine architecture limitations. Theoretically a task and

computational needs assigned to a node can be broken into multiple AWS Lambda

functions, and each function can be run to the maximum concurrent run limit.

This sounds akin to achieving zero idle node.

In reality there is an AWS Lambda concurrency limit, and thus you can’t

let million AWS Lambda function run at the same time and finish the simulation

instantly. However, you can request the concurrency limit increase and it is

worth exploring new architecture by combining additional AWS features and

services. From an architectural point of view, it provides an attractive

opportunity to decouple specific computation task from resources that happened

to be provisioned by an end user.

The following specialized

sets of AWS Lambda functions should be considered:

1.

Market

factor generators, lm

2.

Scenario

generators, ls

3.

Pricing

engines, lp

4.

Aggregation

engines, la

5.

Risk

determinants, lr

Not surprisingly these functions are aligned to what are listed in the

prior section as to how simulation preparation and runs take place. Further,

each set must be completed before proceeding to the next. However, within the

set, asynchronous processing and thus scaling will reduce total processing

time. One thing missing is the customer data sourcing part. This process may

not benefit much from AWS Lambda since such job is typically in persisting once

and reading many times, something typical ETL and data warehousing techniques

can already do a good job. Amazon Redshift sounds perfect for this as it is

designed for OLAP. But the rest of the processes are the core of the time

consuming simulation engine that can be architected very differently than

typical distributed simulation engine.

Besides concurrency limit, there is also a time limit. Based on the

understanding of each specific processing needs, it’s actually hard to imagine

a specialized AWS Lambda function for financial simulation to exceed time limit.

The reason the whole simulation engine takes very long time is driven by

massive number of repeated processes, not really one specific atomic task

taking very long time. Considering the way above AWS Lambda functions are

designed, the behavior should be about the same; each function call should

finish instantly but need to run so many times.

Since AWS Lambda supports dozens of event sources, scheduling of

function calls can be designed in many ways. Amazon SQS for example is one

candidate to invoke functions where within each set of the functions listed

above the job can be completed asynchronously. Since Amazon SQS supports

message attributes that supports string and numeric data type, additional data

can be used by the listener. This can further manage the effective distribution

of the computation tasks. Let’s examine deeper each function.

Considering the subsequent OLAP needs, all the generated data will be

persisted in Amazon Redshift since the usage is write once and read many times.

lm - market factor generators

Preparing end of the day market factors might not be the most

computationally intense task. Further this job needs to be run just once,

unlike processing needs that varies depending on the scenario count. Having

said that there are still opportunities to introduce parallel processing as

it’s not that there is only one specific processing rule that can create all

derived factors. For example computing correlation is totally different from

determining historic volatility of observable market data. Yet the computation

of volatility and correlation may be based on the same data. Therefor

developing specialized AWS Lambda function designed for varieties of market

data preparation is certainly not a bad idea at all. If not for significant

performance boost but at least achieves good component architecture.

ls - scenario generators

Depending on how scenario generation rule is decomposed, there are

varieties of opportunities in creating scenario generators. Similar to the

table shown in prior section (scenario vs. portfolio), scenario generation can

take place via parallel processing. For example, market factors can be grouped

so that across such groups zero correlation can be assumed. Then this presents an

opportunity for asynchronous parallel processing – i.e. invoking many ls at the same time to

complete the task instantly. There’s also a way to logically break into pieces

for more parallel processing. As discussed before, when Amazon SQS is used as a

scheduler, it can include additional attributes. When the attributes are

created in a controlled fashion, then it can further aid in decomposing a

routine into pieces. Consider the following code: for i=1 to 100; process f(i);

next i. Breaking this into two pieces where: 1) for i=1 to 50; 2) for i=51 to

100. It may / may not work but if an Amazon SQS message includes 1/50 vs.

51/101 values, then the function can be run in parallel. Depending on the

specific design of scenario generation there are ample opportunities to run

various ls function in parallel.

lp – pricing engines

Developing pricing libraries and reusing them across distributed nodes

is nothing new. Conceptually this lp function is no different. But the

environment in which this is run is so different than, say invoking FX pricing

function within code run on EC2, it makes a huge difference in efficiency. An

infrastructure that consists of many nodes is as if full of having many bloated

nodes. The benefit of AWS Lambda architecture is expected to be the most

significant from the pricing part. This is because due to the AWS Lambda driven

architecture, the entire pricing part of the simulation engine can be done

across all scenarios and portfolios in an asynchronous fashion. If there is no

concurrency limit at all, theoretically this part, which is the most time

consuming, can finish instantly by running infinite number of lp at the same time.

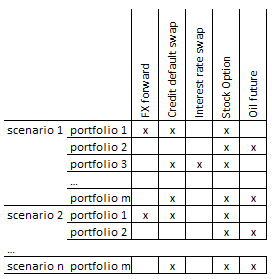

Consider the following table that shows various instruments per

portfolio, and pricing needs across all scenarios:

While traditional distributed computing design can take each “x” mark

and let the scheduler distribute across nodes, it gets very busy quickly and

idle nodes persists. An attempt to decouple components increases scheduler

overhead whereas less scheduler demands creates complex (coupled) big job

assigned to a node that has diversity in resource demands and in completion

time.

AWS Lambda driven way of pricing, however, all “x” marks in the above

table if not constrained by concurrency run limit can be completed

simultaneously without any coordination (scheduling) needs. This is because

each “x” computation has no synchronization needs within pricing step.

Especially that this pricing portfolios across all scenarios is almost always

the most time consuming part of the financial simulation, this could be a major

game changer.

Let’s not also forget that Amazon ElasticCache will aid performance

boost even more. Each specialized function has specific sets of market data

needs, and AWS Lambda is ready to take advantage of Amazon ElasticCache. FX

forward lp has no need for stock market data and oil future lp only needs to worry about

discount rate and related commodity factors. Thus FX forward lp can rely on readily

available FX data in Amazon ElasticCache for its very specific FX pricing

needs.

la – aggregation engine

After all lp complete the jobs, it’s time for the next step - la to begin the process of

aggregation. This process is nothing but aggregating all instruments in a

portfolio to determine the portfolio value for each scenario. Total computation

required depends on number of instruments, portfolio count, and scenario count.

la can

do the bare basic of determining all of portfolio values across all scenarios.

This part again can be done asynchronously, and thus la can be invoked many times

concurrently, reading the data from the Amazon Redshift, to finish the job

extremely quickly.

lr – risk determinants

Typically for the purpose of risk analysis and reporting, expected and

stressed values are produced. Each risk reportable is based on portfolio value

per scenario – the same sets of data produced in the prior step, except how to

use them is different. As such various lr can be defined and they can all run

concurrently to finish the job as fast as possible. One lr will compute expected

portfolio value (average of portfolio value across all scenarios) whereas

another lr will pick 95th percentile and 99th percentile

worst case scenario.

Post processing analysis

All the results, whether a price of an instrument under a specific

scenario, or a portfolio value under another scenario, should be persisted in

Amazon Redshift for subsequent OLAP analysis. As with transaction data, as

various AWS Lambda function computes, it’s all write once and read many times

case. Combined with trade details already in Amazon Redshift, combination of

simulation results also in the same environment enables enormous OLAP analytics

opportunities. For example, tracing of specific one or more instruments or

portfolios across time and underlying factors, and further across scenarios,

are all part of rather plain vanilla OLAP activities. Perhaps after a month or

whenever the OLAP needs decline, data can migrate to Amazon S3, and eventually

Amazon Glacier.

In addition the data whether in Amazon S3 or in Amazon Redshift

presents another analytic opportunities with various Machine Learning (ML)

tools. In order to do ML with financial transactions and market data, you would

have to have the same sets of the data anyway. The whole simulation process

already created such sets.

Practical use

This brand new architecture brings not only decoupling benefits but

also most importantly considerable performance boost. In a way AWS Lambda

architecture makes it a lot closer to achieve the following: today it takes 10

resources 10 hours; tomorrow we run 10,000 resources and finish in 3.6 seconds,

still costing the same in the end.

The idea of eventuality where simulation result becomes instantly

available is totally revolutionary. Today over-night risk processing is typical

and during the day, traders rely on approximation to do their job. Often enough

sensitivity factors are also produced over-night so that during the day without

instant simulation capability, delta and gamma are used to determine

anticipated risk (to be proven after another over-night batch). If the

simulation result is available instantly, however, a trader would input

prevailing rates and gets the results, which will be the most useful.

Given the pay-as-you-go model, a trader will have a discipline in

utilizing such capability. Instead of running one simulation request to another

(since it’s instantly available), the traders are told by finance that each run

cost specific certain amount. This is where detailed cost report by account and

specific cloud resources come in handy. Unless economically makes sense, it

must be discouraged to run whatever it costs to run simulation. The specific

cost will be explicit. Over a very long time, however, the cost will be so low

and the speed is so fast, the simulation engine becomes another cheap utility.

In the U.S. all the major banks are required to submit capital plan

every year per so called CCAR requirements. The deadline for annual submission

does not move yet scenarios regulators release is often delayed. When running

faster is all about provisioning more resources, the cloud architecture and

certainly AWS Lambda simulation architecture is extremely attractive, assuming

scale out is as effective. In a typical scenario, when time to submission

shrinks, planned simulation run will be cut back as it becomes physically

impossible to run very time consuming simulations. The architectural changes

that enables time to complete and pay-as-you-go will dramatically change the

planning and execution.

Perhaps not so fast

For those who consider such AWS Lambda driven reengineering is a

considerable undertaking and thus less dramatic upgrade, or intermediate

reengineering, might be desired. In this section such intermediary architecture

that is a stepping stone to the AWS Lambda based architecture is discussed.

In fact the following steps could be considered a complete cloud

migration strategy; each step bringing in material benefit while at the same

time such staged approach mitigates the risk of huge waterfall that could

break.

1.

On-premise architecture to be migrated to cloud with as little

modification as possible

2.

A job scheduler is replaced by Amazon SQS, and Auto Scaler manages EC2

instance needs

-

Alternatively, or as the next step following SQS based architecture,

develop Elastic Beanstalk application

3.

Jobs performed by EC2 to be replaced by AWS Lambda functions

The first step of just migrating to cloud with little modification

automatically benefits in cost saving. It’s also quite likely to see some level

of performance boost by adding nodes during peak time. The second step is an

intermediary step before full serverless architecture kicks in. Yet this

already has a benefit of decoupling, and benefit of each additional node is

expected to be more than step 1. This is because each node is constantly

processing and as soon as it is done with the job it takes the next available

SQS message and keeps running. It’s quite possible to have significant number

of EC2 instance to be created and concurrent message consumption can be

achieved. Before stepping up to the final stage, Elastic Beanstalk based

application might be an easier step before going to AWS Lambda based. At least

you can take full advantage of managed services. The final step of AWS Lambda

driven architecture is akin to eliminating EC2 from the picture in the second

phase.

My thoughts

Varieties of cloud based simulation documents seem to focus on

migration of existing distributed architecture to cloud. That does have huge

benefits. When seniors learn that on-premise servers are 100% utilized a few

days a month and the rest of the month the usage is under 10%, they have real

hard time keeping all the boxes online doing nothing most of the time. This is

a classic cloud migration benefits.

It turns out at AWS re:Invent 2017, “AWS Lambda for Financial Modeling” talks

about traditional High Performance Computing (HPC) and AWS Lambda based

architecture, which in principle the same as what is discussed in this white

paper. However, this re:Invent presentation talks nothing about specific steps

such as market data preparation, scenario generation, etc. I found the

presentation to be a great intro and thus it is encouraged to watch.

This AWS Lambda based simulation architecture is an elegant one that is

aiming towards massive parallelism that in the end does not cost any extra than

running less slowly. I would like to believe it is a matter of time where we

pay for simulation and the result is available instantly. That certainly

revolutionizes risk management entirely.

The

last update: 12/25/2018

The

page has been designed and written by Ayumi

Ozeki ozekia@gmail.com

go

to home http://ayumi01.s3-website-us-east-1.amazonaws.com